Graphic provided by http://paymycbfbill.com/credit-resources/your-credit-score/.

Credit scoring is a system used to help creditors determine whether to provide you credit, how much credit to offer you, and the terms of your credit repayment. When you apply for any type of credit, such as a loan or credit card, your credit score can either cost you money or save you money. Your credit score is a number between 300 to 850 and is called a FICO score; the higher the number, the better your credit score.

When you have a high credit score, creditors will offer you lower interest rates with more attractive repayment options. On the other hand, if your credit score is lower, you may still be offered credit, but the interest rate will be higher (meaning you will pay more) and the repayment terms will be less appealing.

Credit scores are impacted by the three C’s: character, capital, and capacity.

Character — Is a measure of how a borrower handled past debt obligations. Based upon the borrower’s credit history and personal background, honesty and reliability of the borrower to pay future credit debt is determined.

Capital or Collateral — Refers to how much debt a borrower can comfortably handle.

Capacity — Refers to current available assets of the borrower, such as real estate, savings, or investments that could be used to repay debt if income should be unavailable.

Creditors will also assess your Debt to Income Ratio (DTI). This is your total debt (monthly payments) divided by your monthly income. In general, you should try to keep your DTI lower than 40 percent for a more favorable outcome when applying for credit. Lenders want to know you have enough income to pay all your creditors and if you have low balances you pose less of a risk.

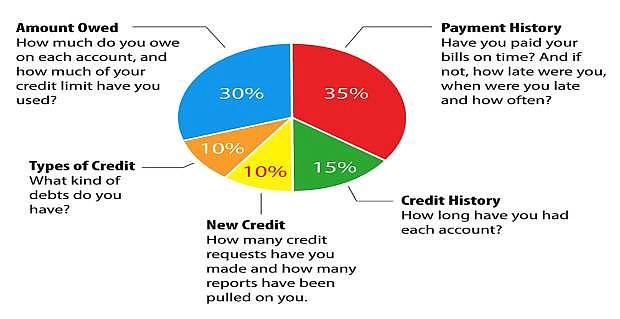

In the credit world, creditors want to know that you will pay them back on time and cause little to no risk when it comes to paying off your debt. The following are factors that impact your credit score and how much they impact that score. While each factor is important, more than half of your score is impacted by the total amount you owe and if you have paid your bills on time.

There are many things you can do to maximize your credit score. If your credit score is low, there is no magical quick fix. Rather, improving your credit score takes time and patience is the key. Following these guidelines will ensure you keep a good credit score or improve your credit score.

Pay your bills on time.

Pay down your debt.

Get your credit report (know where you stand).

Verify that everything listed on your credit report is yours.

Dispute anything on your credit report that does not belong to you.

Pay off collection accounts first and as soon as possible.

Get your debt/credit limit ratio down to 40 percent or less.

Ask for an increase in credit limits, but do not use it.

Keep the oldest credit cards, as longer history means better credit.

In order to establish or have a credit history, you must have borrowed money in the last two years.

Your credit score will decrease with too many inquiries or applying for too much credit at once, carrying high balances, paying late, or garnering collections, liens, or settlements. These negative entries will stay on your credit report for seven years. However, if there are any negative entries on your report that are older than seven years or inaccurate reports, you can contact the credit bureaus, submit a dispute, and request to have it removed. If you need help obtaining a copy of your credit report, you can log into www.annualcreditreport.com to obtain a free copy of your report from the three major credit bureaus — Equifax, Experian, and TransUnion.

Understandably, there are life events or hardships that may cause us to have a credit slip. The most important thing to do is take an assessment of what occurred, review options to redeem the damage or to get back on track, and start paying your debt as soon as possible. You want to prevent slips from becoming collections or wage garnishments, since it will take you longer to rebuild your credit.

To learn more about how to manage your credit, establish or improve and protect your credit, call Financial Guidance Center for a free financial counseling. We can be reached at www.financialguidancecenter.org or by dialing (800) 451-4505 or 775-337-6363. You can also contact Financial Guidance Center to find out how you can apply for Lending Circles to begin to establish positive credit; it is a free program with no fees or interest!

Alma D. De Leon is the Financial Guidance Center’s Northern Nevada director.